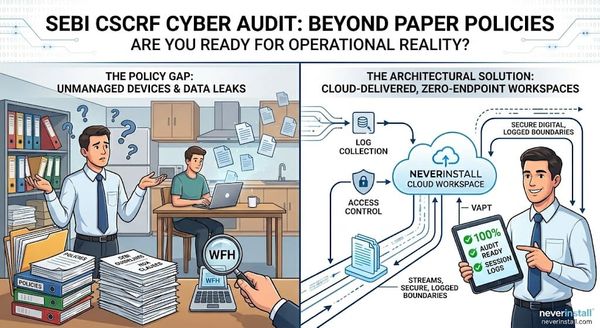

What SEBI's Cybersecurity Framework Actually Means for Your Broking Firm

"The SEBI cyber audit is next quarter." "We're fine. We have policies in place." "What about the dealers working from home? Their devices, the session logs from those terminals?" A pause. "We'll figure it out before then." Walk